Last Updated September 15, 2022

401k plans are mainly for employees of private sector companies. A solo 401k is a 401k for business owners with self-employment income and no non-owner W-2 employees.

Solo 401k Plan Definition

- Solo 401k is a term used to describe an owner-only 401k plan, and has been available since the Economic Growth and Tax Relief and Reconciliation Act (ETRRA) of 2001.

- It is exclusively for the self-employed.

- Other names in the industry used to refer to a solo 401k plan include the following:

Solo(K), Uni(K), Indvidual 401k, self-directed 401k, One-Participant(k), Solo IRA, and Individual (K).

- The solo 401k is more advantageous than a typical 401k plan that is sponsored by employers/companies with multiple employees.

- It is easier to administer and less costly and Congress created it to put owner-only businesses in the same playing field as big businesses that also sponsor 401k plans.

Can Exclude Certain Employees

Under federal laws applicable to qualified retirement plans, specific categories of employees may be excluded from participating in solo 401k plan, which are:

- Employees under age 21

- Employees working fewer than 1,000 hours in a year

- Nonresident aliens

- Union employees

Eligible Solo 401k Employers

- Any type of business entity can sponsor a solo 401k plan provided the business does not employee any full-time non owner employees.

- Businesses that may sponsor a solo 401k plan include the following:

sole proprietors, partnerships, corporations (both subchapter S and C corporations), and limited liability companies (LLCs).

Unincorporated Business Can Sponsor a Solo 401k Plan

- Yes. Unincorporated businesses may use a solo 401k plan provided it does not employee any non-owner full-time employees.

- Also, the self-employed individual’s compensation must be reduced by one half of the social security contribution (Self‑Employment Contribution Act (SECA) deduction.

A Limited Liability Company Can Sponsor a Solo 401k

- Yes, an LLC can sponsor a solo 401k. An LLC is a business that operates with the flexibility and informality of a partnership and yet retains the personal liability protection associated with corporation shareholder interests. For solo 401k purposes, members are treated like partners.

High Contribution limits

- A solo 401(k) allows for the highest contribution limits compared to other retirement account options (e.g., SEP IRA and SIMPLE IRA) for self-employed.

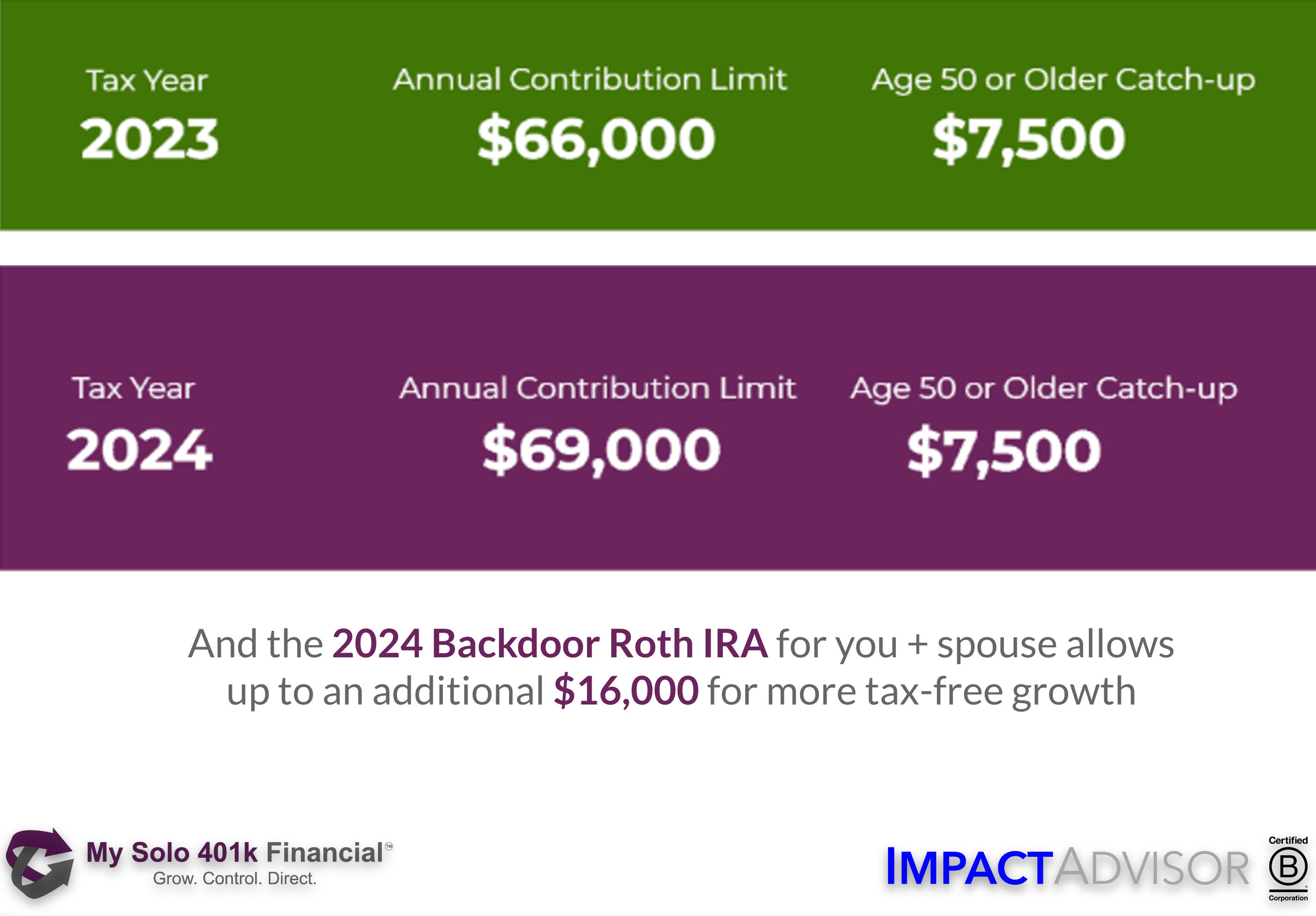

- A solo 401k allows for tax deductible contributions of 25% profit-sharing contribution and salary-deferral contribution of $20,500 for maximum amount of $61,000 per participant for tax year 2022.

- A catch-up employee contribution amount of $6,500 also applies to participant’s age 50 or older.

Roth Contributions

- Roth designated contributions to solo 401k plans are aggregated with pre-tax deferrals for purposes of the elective deferral limit also known as the employee contribution.

- Allows for designated Roth contributions, $20,500 for 2022 plus a catch-up contribution amount of $6,500 for those age 50 or older.

Voluntary after-tax Contributions

- Allows for voluntary after tax contributions of at least $20,500, and up to $61,000 under the overall limit rule.

- Voluntary after-tax solo 401k contributions are not subject to the employee deferral limit (EDL) but are taken into account for the overall contribution limit.

Loans/Borrow

- Resulting from change of IRC Sec. 4975(f) (6), which expanded the loan feature to Solo 401k plans, participants can borrow from the Solo 401k.

Incoming Transfers/Rollovers

- Allows for incoming rollovers/transfers from other retirement plans (e.g., 401ks, profit sharing plans, 403(b)s, define benefit plans, 457s and Standard IRAs).

- Annual Contributions not required–business owners can contribute in some years but are not required to contribute every year.

Easy to Administer

- Even though Solo 401k plans are 401(k)-based plans, they are easier to administer because they are not subject to the majority and costly nondiscrimination testing that apply to regular 401(k) plans.

Reporting: Form 5500 EZ

- A solo 401k plan is eligible to file Form 5500-EZ, Annual Return of One-Participant (Owners and Their Spouses) Retirement Plan.

- No Form 5500-EZ reporting is necessary as long as plan assets at the end of the plan year do not exceed $250,000. All of your other owner-only plans (e.g., other solo 401k plans as well as defined benefit plans) must be aggregated for purposes of the $250,000 limit.

- A final Form 5500-EZ must be filed (even if the value of the plan is less than $250,000) for the final plan year whether or not the plan was required to file a Form 5500-EZ for any prior year.

Plan Trust Document

- In order to establish aSolo 401k plan, the employer is required to fill out and sign a written, plan trust document that has been approved by the IRS.

Bank or Brokerage Account for Self-Directed Accounts

- For those who open a solo 401k with the self-directed option, either a bank or a brokerage account can be opened in the name of the solo 4o1k plan for placing investments.

- They both come with checkbook and wire control.

- The brokerage account comes with checkbook and wire control and is also one stop shop in that you can also invest in equities. On the other hand, the bank account does not allow for investing in equities. COMPARISON

Use Solo 401k or Solo 401k LLC for Placing Investments

- Real estate investments can be made directly through the solo 401k plan, which is the most common method, or through a solo 401k owned LLC (often referred to as a solo 401k llc).

- With respect to protection from creditors, if the real estate investment is made directly through the solo 401k plan, property insurance is often purchased for protection. Also, protection from creditors for a solo 401k falls at the state level.

Invest in Options

- A solo 401k plan may be invested in options and margin may be used.

- While a Solo 401k can invest on margin, income derived from margin trading is subject to UBIT.

- Option strategies such as covered calls and covered puts have no margin requirement since the underlying stock is used as collateral. If the solo 401k brokerage account has been approved for margin but the margin account is not being used then Unrelated Business Income Tax (UBIT) would not apply.UBIT is triggered when the margin account is being utilized.

Distributions

- While distributions from 401k plans (e.g., full-time employer 401k plans) are generally only available at separation from sevice or death, the solo 401k plan distribution events are more plentiful. For example, IRAs or former employer 401k plans funds that were transferred to the solo 401k plan can be distributed at any time, regardless of age.VISIT HERE to learn more.

- Unless anexception applies, there is a 10% penalty on solo 401k distributions if the participant is under age 59½.

Required Minimum Distributions

- For Solo 401k plans, required minimum distributions (RMDs) must commence for the year the participant attains age 72.

- COMPLIANCE NOTE: Don’t confuse the “still-working exception” rule that applies to employees who participate in full-time employer 401k plans who do not own more than 5% of the company and can thus defer RMDs from the 401k plan offered by the employer that they work for until the year they separate from service or retire. This “still-working exception” rules does not apply to solo 401k plans because the it is a plan for owner-only businesses.

- RMDs from 401k plans including solo 401k plans cannot be aggregated. This means that RMDs for each 401k must be calculated separately and taken separately from each plan. Lastly, solo 401k RMDs cannot be distributed from IRAs and vice versa.

- Visithere to learn more about solo 401k RMDs.

Creditor Protection in Bankruptcy

- Solo 401k participants who have declared bankruptcy are fully protected from creditors going after their solo 401k plans.

Creditor Protection Outside Bankruptcy

- A solo 401k plan is a non-ERISA plan, which means it receives protection at the state level not the federal level. In order to receive creditor protection at the federal level, the business sponsoring the solo 401k plan would need to employ non-owner W-2 employees who also participate in the 401k plan, which is not possible for a solo 401k plan because only owner-only businesses with no full-time W-2 employees can adopt a solo 401k plan.

Participation in a Solo 401k (or SEP) May Impact Pretax IRA Contributions for You/Spouse

- While the IRS rules allow for contributions to both Solo 401k plans and IRAs, if you are also participating in a solo 401k plan, you can still make the traditional IRA contributions but they may not be tax deductible. IRS income limits for IRA deductibility when you oryour spouse are covered by a workplace plan.

Contributions (pretax, Roth and voluntary after-tax) are Based on Earned Income NOT Passive or Investment Income & Can’t Contribute More than You Make

- Whether making some or all threetypes of solo 401k contributions (i.e., Roth, Pretax and Voluntary After-Tax), you must have earned income from self-employment not investment or passive income. For example, if your self-employed business is taxed as an S-corporation, solo 401k contributions would be based on your W-2 wages from the self-employed business-not your pass-through income. See Revenue Rulings 71-26 and 59-221.

- Also, you can’t contribute more than you make. The annual additions may not exceed the lesser of 100 percent of your compensation from self-employment, W-2 in the case of an entity taxes as an S-corporation, for example, or $58,000 for 2021 and $61,000 for 2022. This allocation limit applies to all three contribution sources including employer profit sharing contributions.

Not Registered with the State

- A solo 401k plan is not registered with the state even though it falls under the retirement trust umbrella. Since the 401k is not a business entity, it will not show up on the secretary of state website. Solo 401k plan documents are not submitted to the Secretary of State

Custodian of the Solo 401k Fund

- With a solo 401k, the trustee (the business owner) decides on the financial institution to hold the solo 401k funds. We have helped clients open accounts at 100s of different banks and many brokerages (including Interactive Brokers, Fidelity, Schwab, and E-TRADE, to name a few) and we would do the same for you.

Mark Nolan, Founder, COO: My Solo 401k Financial

- Each day I speak with energetic entrepreneurs looking to take the plunge into a new venture and small business owners eager to take control of their retirement savings. I am passionate about helping others find their financial independence. Having worked for over 20 years with some of the top retirement account custodian and insurance companies I have a deep and extensive knowledge of the complexities of self-directed 401ks and IRAs as well as retirement plan regulations.

Learn more about Mark Nolan and My Solo 401k Financial

{kind=link}